The monetary policy operational framework of the Bank of Botswana is implemented through Open Market Operations (OMOs). These operations aim to maintain liquidity conditions and short-term interest rates consistent with the monetary policy stance determined by the Monetary Policy Committee (MPC).

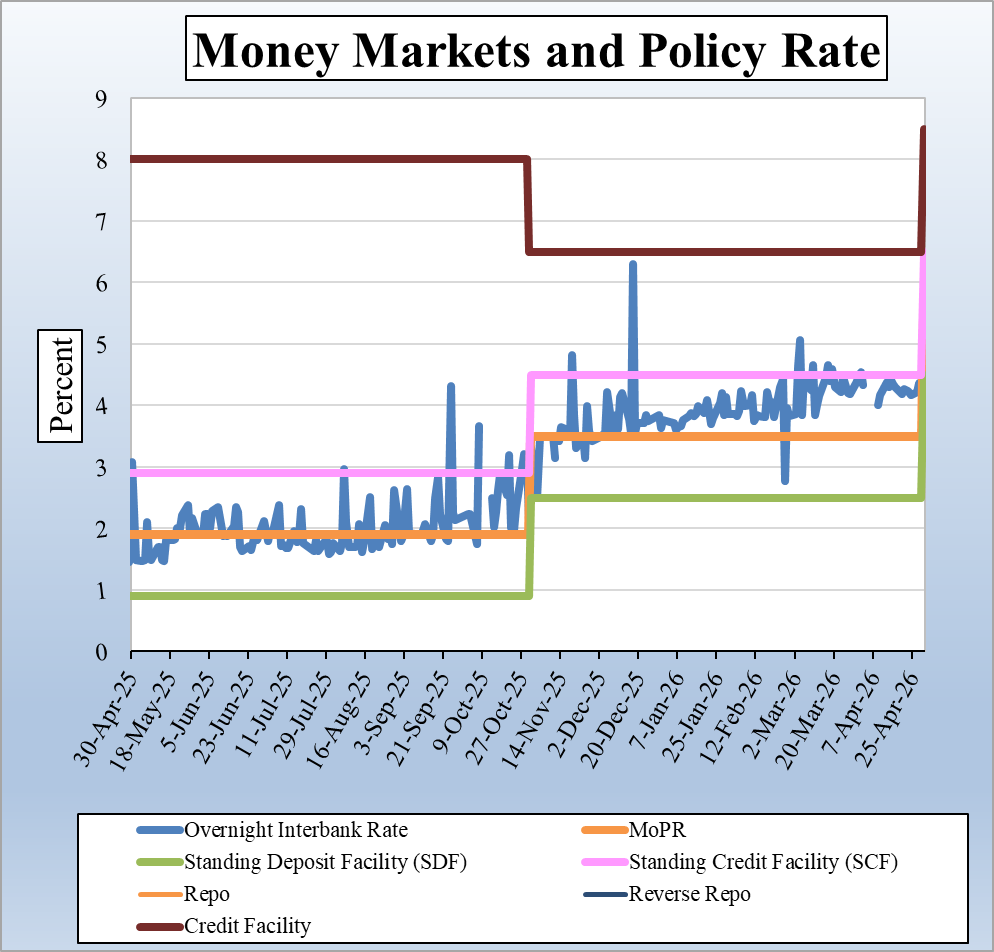

The Bank’s primary instruments for open market operations are Bank of Botswana Certificates (BoBCs), which are used to manage liquidity and influence short-term market interest rates. The Bank currently issues 7-day and 1-month BoBCs. In support of this framework, it operates an interest rate corridor of 200 basis points around the Monetary Policy Rate (MoPR), with the Standing Deposit Facility (SDF) set at 100 basis points below the MoPR and the Standing Credit Facility (SCF) at 100 basis points above it, to support commercial banks’ day-to-day liquidity management. The Bank also conducts discretionary fine-tuning operations, including repos and reverse repos, at the prevailing MoPR to smooth liquidity conditions in the banking system. In addition, a secured Credit Facility is available to commercial banks for intraday and overnight liquidity management.

Effective conduct of OMOs requires continuous forecasting of market liquidity conditions. In this regard, the Bank publishes a range of money market data, including BoBC auction results, which are made available through its website and statistical publications.

At its meeting of 30 April 2026, the MPC increased the MoPR by 200 basis points from 3.5 percent to 5.5 percent, as part of a policy recalibration aimed at strengthening policy transmission, while maintaining the directive that commercial banks should not increase Prime Lending Rates (PLRs). Consequently, the SDF rate is set at 4.5 percent (100 basis points below the MoPR), while the SCF rate is set at 6.5 percent (100 basis points above the MoPR), thereby helping to anchor short-term market rates.

Primary Reserve Requirements

The Bank is empowered, under Section 40 of the Bank of Botswana (Amendment) Act, 2022, to impose a Primary Reserve Requirement (PRR) on commercial banks. A bank’s PRR is calculated based on its reservable liabilities in the month preceding the start of the current Reserves Maintenance Period (RMP). Reservable liabilities comprise Pula-denominated customer deposits and exclude interbank deposits and securities issued by commercial banks. PRR balances are not remunerated, and vault cash does not qualify towards meeting the requirement.

PRR balances, where applicable, are maintained on an average basis over the RMP, which runs from the second Wednesday of a month to the second Tuesday of the following month. During this period, banks may freely transfer balances between their PRR accounts and Settlement (current) Accounts during Botswana Interbank Settlement System (BISS) operating hours.

Any shortfall in the PRR balance attracts a statutory penalty of up to 0.2 percent per day on the deficiency.

At its meeting of 5 December 2024, the MPC reduced the PRR from 2.5 percent to 0 percent, effective 11 December 2024, to address structural liquidity constraints in the banking system.

Open Market Operations (OMOs)

The Bank conducts the following regular OMO instruments:

• 7-day BoBCs are auctioned weekly (Tuesdays) on a Fixed Rate Full Allotment (FRFA) basis at the MoPR, with T+1 settlement.

• 1-month BoBCs are auctioned on the third Tuesday of each month, for a predetermined volume on a multiple-price basis, with T+1 settlement.

In addition, Fine-Tuning OMOs (FTOs) may be conducted on an ad hoc basis, typically overnight, at the MoPR, with T+0 settlement, and executed through repo or reverse repo transactions.

Results of OMO operations are published on Bloomberg, Refinitiv, and the “Latest News” section of the Bank of Botswana website.

Standing Facilities (SF)

The standing facilities framework provides a corridor system around the MoPR to anchor short-term interest rates:

• Standing Deposit Facility (SDF): Overnight deposits at MoPR less 100 basis points (currently 4.5 percent), with T+0 settlement.

• Standing Credit Facility (SCF): Overnight lending at MoPR plus 100 basis points (currently 6.5 percent), with T+0 settlement, conducted on a repo basis.

The SCF is available during BISS operating hours (up to 17:30), while the SDF is accessible until 18:15.

The Bank also provides a Credit Facility (CF) to prevent settlement account overdrafts. This facility offers overnight funding at MoPR plus 300 basis points, with T+0 settlement, against pre-pledged collateral.

In addition, intraday credit (daylight exposure) is available to support payment system efficiency. This facility is interest-free if repaid within the same business day; otherwise, it is automatically converted into overnight CF borrowing.

Eligible Counterparties

All commercial banks authorised and operating in Botswana are eligible to participate in the OMOs, and to make use of the CF, subject to the appropriate legal agreements.

Lender of Last Resort

In accordance with Section 38 of the Bank of Botswana (Amendment) Act, 2022, the Bank may, under exceptional circumstances and on terms it deems appropriate, act as lender of last resort by extending credit to solvent but illiquid banks for a period of up to 92 days.

Eligible Collateral Pool

Eligible collateral for the Bank’s ] operations comprises:

• Bank of Botswana Certificates (BoBCs);

• Government of Botswana Treasury Bills and bonds; and

• Corporate bonds listed and traded on the Botswana Stock Exchange.

Of the eligible collateral, Government securities and corporate bonds are subject to valuation haircuts based on residual maturity,on the current market valuation. A haircut refers to the lower-than-market value placed on an asset being used as collateral for a loan.

Commercial banks are allowed to pre-pledge collateral to the Bank up to 150 % of their core capital, ensuring immediate access to liquidity facilities when required.

Legal Documentation

Repo transactions (Finetuning operations and SCF) between the Bank and commercial banks are subject to a Master Repurchase Agreement, while intraday credit and CF borrowings fall under a pledged collateral agreement.